DarioGaona

While the gold and also silver miners have actually taken pleasure in a multi-month rally, and also this outperformance vs. various other indices has actually proceeded right into 2023, First Majestic ( NYSE: AG) has actually been the typical runt of the trash. This is shown by its unfavorable year-to-date efficiency and also December return vs. a double-digit favorable return for most of its peers. The factor? Not just did the business have a difficult Q4 operationally, yet its FY2023 overview has actually left a lot to be wanted, and also the turn-around at Jerritt Canyon is relocating slower than some had actually really hoped. As a matter of fact, the possession will certainly be fortunate to create 130,000 ounces this year, recommending the 200,000-ounce per year objective can be extra evasive than formerly prepared for.

Commonly, a difficult quarter or softer full-year assistance can be a possibility to get a top notch name as it relocates onto the sale shelf. Nonetheless, in the instance of First Majestic, its assessment remains to be abundant about what financiers are obtaining for that rate. Worse, the brief and also medium-term overview concerning changing books does not show up to have actually ended up being anymore beneficial after 2 years of inflationary stress, while the silver rate has actually had a hard time to continue to be over $22.00/ oz on a lasting basis. Allow’s take a more detailed look listed below:

Jerritt Canyon Mine Procedures ( Business Discussion)

Q4 & & FY2022 Manufacturing

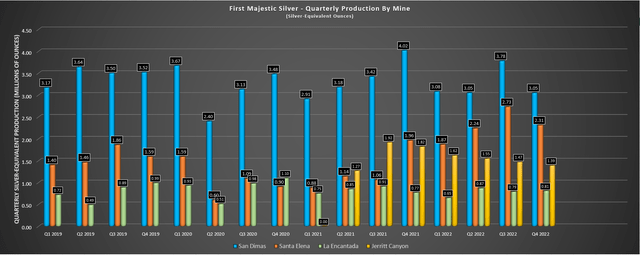

Very first Majestic Silver launched its Q4 and also FY2022 results today, reporting quarterly manufacturing of|2.40 million ounces of silver and also|63,00 ounces of gold. This stood for an 18% decrease in silver manufacturing on a year-over-year basis, with manufacturing affected by the reduced silver qualities at Santa Elena, where ore feed is primarily from Ermitano (gold-rich vs. silver-rich), with 80% of tonnes from the mine in Q4. At The Same Time, San Dimas saw a sharp dip in result year-over-year (3.05 vs. 4.02 million ounces), with the possession up versus hard compensations year-over-year, affected by reduced quality growth ore from the Perez capillary. Throughout the quarter, qualities balanced 220 grams per tonne of silver and also 3.12 grams per tonne of gold, below 347 grams per tonne of silver and also 3.71 grams per tonne of gold in Q4 2021.

Initial Majestic Silver – Quarterly Manufacturing by Mine ( Business Filings, Writer’s Graph)

Transferring To La Encantada, manufacturing was available in at|805,000 ounces of silver, a 5% rise over prior-year degrees. This was aided by somewhat much better qualities and also greater silver healings, countered by a dip in tonnes refined. The bright side is that qualities must enhance by Q2 2023 with stope ore offered from the Beca-Zone orebody. Generally, this led to a blended year for its Mexican silver procedures, with an outstanding year from Santa Elena (81% rise in silver-equivalent manufacturing) aided by Ermitano, countered by a weak year at San Dimas and also greater prices as a result of inflationary stress. On the other hand, the business’s latest procedures hindered via the year, and also it upright a reduced note, particularly thinking about that Q4 was meant to be a lot more powerful for the Nevada possession, as reviewed in the Q3 ready comments (revealed listed below).

” Nonetheless, we remain to prepare for a solid recuperation at Jerritt Canyon in the 4th quarter and also right into very early 2023 as Smith Area 10, West Generator and also Saval II mines come online in November. The addition of these brand-new manufacturing locations are anticipated to boost ore shipments to 3,000 tpd and also significantly lower prices.”

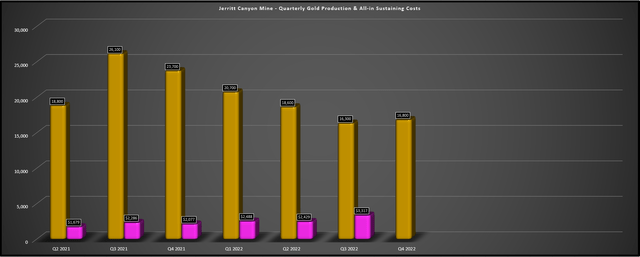

Sadly, not just was Q4 not a peak, it was near the nadir for the quarter, with a meager 1,951 tonnes each day refined at qualities well listed below my price quotes. The outcome was that the mine created simply|72,400 ounces in FY2022 and also simply|140,000 ounces considering that being obtained yet at all-in-sustaining prices [AISC] that have actually balanced about $2,000/ oz. In previous updates, I kept in mind that there was marginal worth in evaluating this possession throughout its turn-around stage which it dealt with an absence of correct financial investment under previous proprietors. Rather, a much better court of its capacity would certainly be the 2023 and also 2024 outcomes as soon as Very first Majestic had actually invested effectively on enduring resources and also had time to maximize the possession.

Jerritt Canyon Mine – Manufacturing & & All-in Sustaining Prices ( Business Filings, Writer’s Graph)

Nonetheless, evaluating by the 2023 assistance of 119,000 to 133,000 ounces at a $1,780/ oz AISC mid-point, this turn-around can take longer than I prepared for, and also the business’s comments at the time of the procurement look extremely enthusiastic, at the very least in regards to the timeline supplied. Allow’s take a closer appearance:

Jerritt Canyon Disappoints

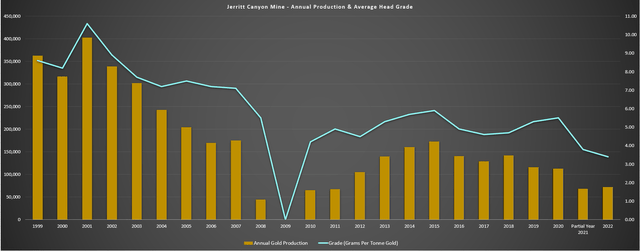

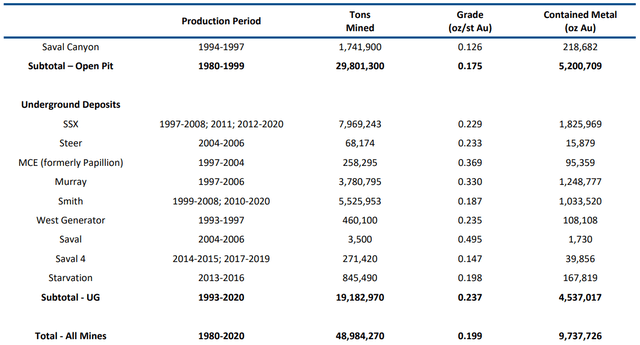

Taking a look at the graph below, Jerritt Canyon has actually seen a substantial decrease in yearly manufacturing and also qualities considering that the millenium, going from a 300,000-ounce-per-annum procedure to having a hard time to work up a 150,000-ounce year over the previous years. Sadly, the previous 2 years under First Majestic have not caused any type of modification in this pattern, with mixed manufacturing from a partial year in 2021 and also 2022 being available in listed below 150,000 ounces incorporated As we can see, this dip in manufacturing has actually been grade-driven, with qualities gliding to 3.80 grams per tonne of gold in 2021 and also 3.4 grams per tonne of gold in 2022, below 10.0+ grams per tonne of gold in 2001.

Jerritt Canyon Mine – Historic Manufacturing ( Business Filings, Writer’s Graph)

At the time of the procurement, First Majestic’s administration mentioned the following:

” This possession has actually not had a major financial investment in establishing our growth or expedition for virtually 20 years or thereabouts. It made use of to be run by Freeport back in the 80s. It was a collection of open pits. They obtained diminished at those steel rates. Today we believe those pits can be resumed at the existing steel rates, which we’re currently reviewing, and also we’re anticipating to increase the manufacturing below over the following number of years. We’re in fact anticipating to have, in 2024, we’re anticipating 200,000 ounces of gold – contrasted to 110,000 ounces this year (2021 ).”

– Gold Online Forum Americas, First Majestic Discussion

Plainly, the 2021 manufacturing objective did not fulfill assumptions with a sub-100,000- ounce year for manufacturing, and also wagering versus the overview of 200,000 ounces in 2024 pertaining to fulfillment at this moment has to do with as near complimentary cash as one can obtain if a wager were offered. This is since the only means this will certainly take place is if the business refines at a price of at the very least 4,000 bunches each day and also a 5.50 gram per tonne ordinary quality, and also it would certainly still likely show up reluctant of this number making use of 84% healings (| 197,000 ounces vs.|200,000 ounces). As a matter of fact, while the business shows up honored to reveal the|70% rise in manufacturing year-over-year at the mid-point, this number is miles listed below where this possession was directed to be from a tempo perspective if it were to create 200,000 ounces in 2024.

All that being stated, there are some indicate unload, and also while the 200,000-ounce objective by 2024 is much also enthusiastic, 2022 will likely be the nadir for this possession.

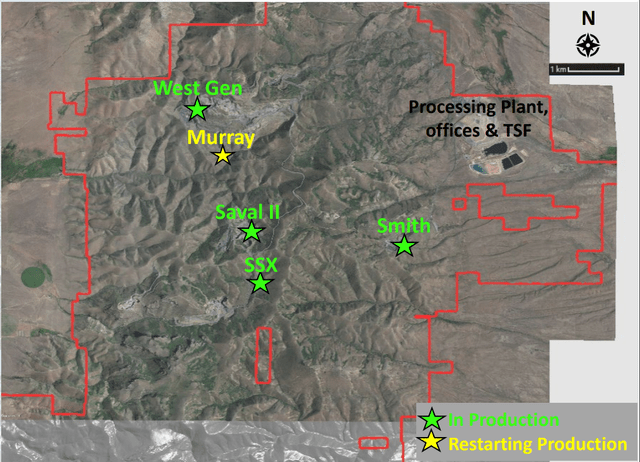

Jerritt Canyon – Plant, Mines & & Targets ( Business Discussion)

For beginners, Q4 was an extremely challenging quarter from a climate perspective in Nevada, with numerous weeks of extreme winter in North Nevada and also dual typical snowfall quantities that made ore haulage extra tough from its SSX and also West Generator mines. The map over programs that these mines exist even more from the plant than Smith. So, also if extracted tonnes boosted in Q4 to utilize repaired prices at the possession (substantial excess ability of 4,000+ bunches at the plant), it does not assist if those tonnes can not effectively make it to the plant to be dealt with to provide the anticipated ore manufacturing. Some financiers may keep in mind that this is simply a practical reason, yet I would certainly differ and also believe the business is worthy of a hand down the weak Q4 outcomes.

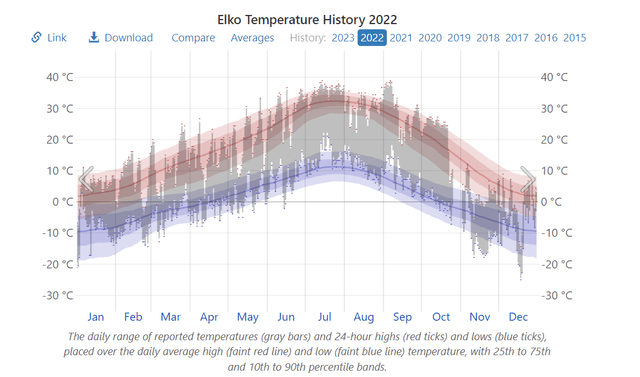

The weather condition in Elko, Nevada, is revealed listed below, and also it’s clear that November and also December 2022 were much cooler than previous years, taking a look at the dataset, with temperature levels constantly listed below 10 celsius and also diving listed below [-] 20 celsius on greater than one event.

December 2022 Elko Temperature Level Background vs. Balances ( WeatherSpark.com)

Second Of All, and also in First Majestic’s protection, this is a property performing at hardly 50% of its ability (4,000+ bunches each day), yet the business is ultimately supplying on its objective of bringing brand-new mining facilities to make use of the considerable ability at the plant, comparable to the mining complicated design that Barrick (GOLD) utilizes in Nevada. This consists of finishing the second getaway method the West Gen Mine to boost ore manufacturing, increase the higher-grade Smith Area 10, and also it’s working with increase manufacturing from the formerly shuttered Saval II Mine that rests simply north of SSX. The outcome is that we must have 4 mines feeding the plant in 2023 vs. 2 in 2021, and also the qualities out of Smith must be much better, with accessibility to greater qualities in between the SSX and also Smith Areas.

The outcome of this job is that we must see a lot greater qualities in H1 2023 at Jerritt Canyon, and also the objective is to have actually extracted qualities of|5.4 grams per tonne of gold for FY2023, converting to a feed quality simply reluctant of 5.0 grams per tonne of gold. Presuming an 83 – 84% recuperation price, this must equate to 120,000 plus ounces per year and also below $1,800/ oz AISC, a purposeful renovation from FY2022 degrees ($ 2,000/ oz plus AISC). On the other hand, the business is wanting to reactivate the top-quality Murray Underground Mine (1.24 million ounces created traditionally at 10+ grams per lots of gold), giving added step-by-step feed beginning following year. Presuming a 6.0 gram per bunch quality and also a payment of 700 bunches each day, this can include an additional 35,000+ ounces to what seems a manufacturing account of|125,000 ounces per year.

Jerritt Canyon – Historic Manufacturing ( Technical Record 2021)

So, while this possession absolutely does not motivate any type of self-confidence based upon its 2021 and also 2022 manufacturing, First Majestic has actually made substantial progression that isn’t appearing in the Q4 or FY2022 outcomes, and also maintaining resources has actually risen in this duration, with $55+ million invested considering that the task was obtained. Consequently, while the 2023 assistance was listed below my price quotes from a manufacturing perspective (| 140,000 ounces) and also well over my assumptions of sub $1,700/ oz AISC from a price perspective (real assistance: $1,733/ oz to $1,842/ oz), 2024 has the possible to be a better year.

To sum up, the most awful outcomes seem in the rear-view mirror at Jerritt Canyon, and also I continue to be carefully positive concerning this possession. That stated, I believe an extra conventional overview is 140,000 to 155,000 ounces per year (post-2024) at below $1,700/ oz AISC vs. the overview supplied at the time of the procurement of|200,000 ounces per year at what would certainly have been sub $1,500/ oz AISC. Furthermore, I would certainly be remiss not to keep in mind from an adverse perspective, get substitute can be extra tough than anticipated as a result of inflationary stress, with the opportunity that the cut-off quality at the possession can boost in the direction of 4.6 grams per lots of gold (formerly:|4.4 grams per lots of gold in the 2021 Technical Record), also if the business readjusts its gold rate presumption to $1,550/ oz or greater from $1,500/ oz presently.

Placing Everything With Each Other

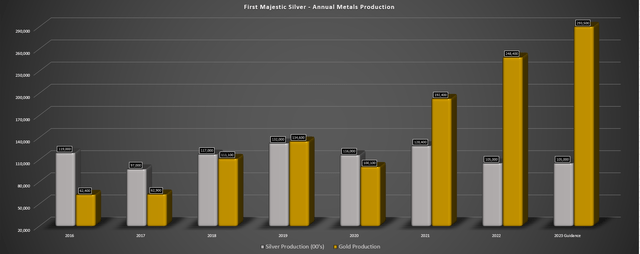

Offered the softer year vs. what I anticipated at the business’s Jerritt Canyon Mine and also reduced silver manufacturing at Santa Elena, where mining will certainly be only concentrated on the higher-grade Ermitano ore, First Majestic anticipates to create|293,000 ounces of gold and also|10.6 million ounces of silver. This would certainly equate to silver manufacturing continuing to be at multi-year lows (2021:|12.8 million ounces), countered by a substantial rise in gold manufacturing, which would certainly boost 120% over 2019 degrees (| 135,000 ounces created). Nonetheless, although manufacturing is relocating the ideal instructions, the pattern in manufacturing per share has actually been much less remarkable, affected by considerable share dilution from the Jerritt Canyon procurement.

At The Same Time, from a combined price perspective, First Majestic’s all-in-sustaining prices per silver-equivalent ounce [SEO] are anticipated ahead in at $18.47/ oz to $19.72/ oz, giving little margin for mistake if we presume an extra conventional silver rate of $22.00/ oz for the year. Worse, these prices are up significantly from FY2022 assistance (which the business will certainly miss out on as a result of manufacturing deficiencies in Q4), which was evaluated $17.68/ oz to $18.42/ oz. So, while combined manufacturing might boost 10% year-over-year in 2023, the greater price account greatly offsets this.

The outcome is that First Majestic Silver is truly ending up being First Majestic Gold (an adverse growth considered that gold manufacturers commonly trade at reduced multiples), and also the business has razor-thin margins till Jerritt Canyon is maximized post-2023, or unless steels rates boost significantly. Therefore, I do not see any type of hope of this supply going back to the $13.00 per share degree at any time quickly, not to mention $17.00. This indicates that numerous silver apes that hurried right into the supply to take part in the silver capture guarantees by some experts are most likely to produce above resistance for the supply and also bring about sharp rallies being offered as these ended up being impatient after holding a shedding financial investment, while various other silver manufacturers at the same time surpass.

Evaluation & & Technical Photo

Based Upon|286 million shares exceptional and also a share rate of US$ 8.10, First Majestic trades at a market cap of|$2.32 billion. Also after the current share-price decrease, this still contrasts adversely with an approximated web possession worth of $980 million. As a matter of fact, after separating Very first Majestic’s market cap by its approximated web possession worth, we can see that the supply has among the highest possible multiples sector-wide, trading at virtually 2.30 x P/NAV. This is in spite of|70% of income originating from a Tier-2 territory (Mexico). And also, the business currently has a better percentage of income from gold which must reduce the costs numerous it regulated in 2016 as a result of being mainly a silver manufacturer.

Adhering to the procurement of the Jerritt Canyon Mine and also the greater gold qualities at Ermitano vs. Santa Elena, First Majestic’s portion of income originating from gold has actually boosted significantly vs. 2016 degrees (revealed listed below).

Initial Majestic Silver – Yearly Metals Manufacturing & & 2023 Support ( Business Filings, Writer’s Graph)

Historically, I have not located any type of worth in paying greater than 1.25 x P/NAV for a gold/silver miner. The only exemptions are when stated business is a typical unicorn (industry-leading margins, high double-digit manufacturing development, and also all procedures in Tier-1 territories), like Kirkland Lake Gold was from 2017-2019. This is absolutely not the instance with Very first Majestic, whose just Tier-1 territory possession has actually underperformed assumptions; its combined AISC margins are listed below 20% at an extra conventional $22.00/ oz silver rate, and also it will certainly be fortunate to expand yearly manufacturing by greater than 10% this year. So, with First Majestic remaining to trade at one of the highest possible P/NAV multiples sector-wide, I remain to see absolutely no margin of safety and security from an appraisal perspective.

The bright side is that an increasing trend will certainly raise all watercrafts, and also while Very first Majestic had a harsh year in 2022 with considerable misses on assistance, it ought to see a renovation in margins if the gold and also silver rates can proceed their higher trajectory. Nonetheless, also if this holds true, the objective ought to be to get top notch firms that constantly provide on pledges at a deep discount rate to reasonable worth. Pertaining to turn-arounds or firms that have actually battled to fulfill pledges, one must require an extra considerable margin of safety and security to make up for the unfavorable belief that can consider on the supply, the reduced likelihood of remarkable implementation, and also the greater threat. Considered That First Majestic suits the 2nd classification yet is among one of the most costly, I do not see any type of means to validate being long below at US$ 8.10.

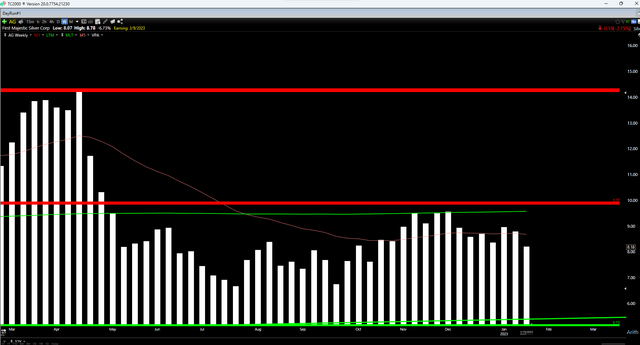

AG Weekly Graph ( TC2000.com)

Ultimately, if we consider the technological image, we can see that while AG has actually drawn back greatly from its current highs, it’s still being in the top part of its anticipated support/resistance variety. This is based upon the supply having no solid assistance till the US$ 5.15 – US$ 5.35 area and also solid resistance expenses at US$ 9.90 to US$ 10.10. If we gauge from an existing share rate of US$ 8.10, this equates to $2.75 in possible disadvantage to sustain and also simply $2.00 in possible benefit to the top side of resistance, converting to a reward/risk proportion of 0.73 to 1.0. I choose a minimum of a 5.0/ 1.0 reward/risk proportion to validate beginning brand-new placements in small/mid-cap names, suggesting that AG is still not in a low-risk buy area and also would certainly require to dip listed below US$ 6.00 to come to be extra fascinating.

Recap

While First Majestic has actually directed for a better year in advance, the overview was well listed below my previous price quotes. Furthermore, while I was carefully positive concerning Jerritt Canyon being|170,000-ounce manufacturer at sub $1,450/ oz AISC in 2024, I’m much less positive in this overview based upon what’s been stickier rising cost of living than anticipated. And also, including books can be harder than formerly prepared for, considered that cut-off qualities must boost vs. the 2021 record. So, while this possession can create a good quantity of capital in a $2,000/ oz+ gold rate setting, despite an extra conventional overview of 145,000 ounces per year annualized run price beginning in Q2 2024 at sub $1,650/ oz AISC, the possession’s future is a lot less glowing in a weak gold rate setting (below $1,800/ oz).

To sum up, the one item of this tale that can bring about a re-rating (Jerritt Canyon in Nevada) hasn’t met assumptions, and also I do not anticipate get substitute to obtain a lot easier for silver manufacturers as a whole (neither Jerritt Canyon), with inflationary stress affecting cut-off qualities in any way procedures. On the other hand, although manufacturing is increasing, prices are increasing in accordance with prices, and also after a harsh year of missing out on price quotes, the marketplace might be much less nervous to appoint the costs numerous the supply has actually regulated in previous years. Therefore, with First Majestic trading at a costs to various other rare-earth elements names, I remain to see restricted loved one worth in the supply, recommending the supply is best to Prevent unless we see a lot reduced rates.