")

spooh

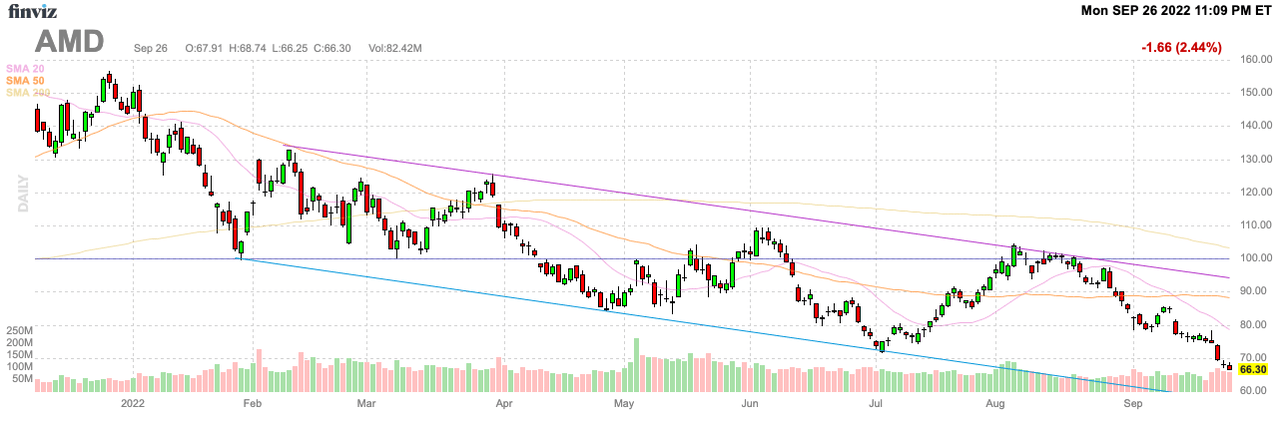

Abruptly, Superior Micro Units (NASDAQ:AMD) trades beneath $70 regardless of no proof the corporate is going through critical discount to development targets. Just a few analysts have reduce monetary estimates in restricted discount to expectations, principally on account of a weak PC market. My funding thesis is extremely Bullish on the inventory buying and selling beneath $70 on account of long run development drivers.

Supply: FinViz

Powerful Market

Numerous chip firms have lowered estimates, however a variety of the main firms have maintained sturdy development for the 12 months. The auto and server markets stay sturdy, even with a looming world recession.

In line with Morgan Stanley, AMD will miss monetary targets on account of a weak PC market. The chip firm has already highlighted the lack to satisfy demand within the server market and for the Xilinx product line. AMD has struggled to provide sufficient chips to even concentrate on the bottom PC market hit by covid pull forwards going through a tricky market dynamic. The key affect of the PC weak point has hit Intel (INTC) flush with low-end chips.

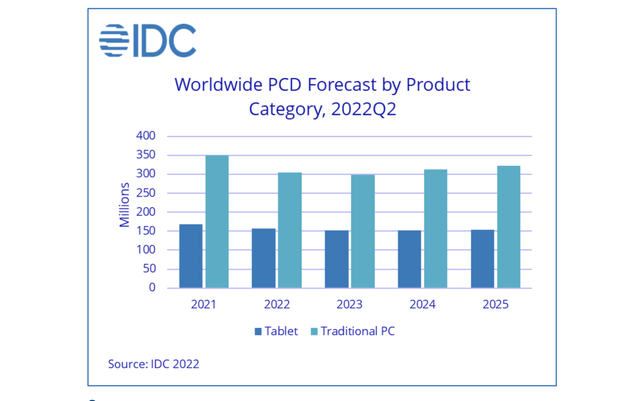

IDC forecasts conventional PC shipments to fall 12.8% in 2022. The analysis agency even forecasts a minor dip in 2023 earlier than the business rebound in 2024/25.

Supply: IDC

The important thing right here is that almost all of the declines come within the client sector the place low-end PCs are purchased. The enterprise section is forecast at comparatively flat.

Regardless, analyst Joseph Moore reduce the AMD EPS targets to $4.02 in 2022 and $4.40 in 2023. The analyst reduce $0.22 and $0.32 off the prior estimates, respectively. Morgan Stanley was already beneath the consensus estimates by roughly $0.15 for annually.

One has to comprehend that this analyst was already typically damaging on the numbers offered by AMD. The consensus income estimate is now down to simply $26.2 billion whereas the corporate supplied up a view of $26.3 billion when reporting numbers on the finish of July.

AMD attended a number of conferences not too long ago with no trace of weak point the corporate would not overcome. Forrest Norrod, Sr. VP of Datacenter and Embedded Options, spoke of an inflection level within the cloud and hyperscalers and robust momentum within the enterprise section, with no indicators of a slowdown:

However I feel we’re going to continue to grow and taking share actually unbiased of the setting.

The manager continued to talk of provide constraint points

Yeah. I feel for us now we have been utterly — within the Knowledge Middle enterprise, now we have been utterly provide gated for fairly a while. So we’re — our development is totally modulated by provide. And it’s not wafer provide, we are able to get all of the silicon, we’d like our partnership with each TSMC and GLOBALFOUNDRIES, it has been nice and people guys have been very responsive.

For us, it’s actually about substrates. So the underappreciated piece of fiber glass and metallic that join the chips encapsulate the silicon dye and join them to the motherboard. That’s been the constraint… these substrates are a little bit bit less complicated to fabricate and that constraint, I’d say, is gone for the remainder of the enterprise by the top of the 12 months. However for servers, I feel, we’re nonetheless going to be considerably modulated by that into subsequent 12 months, however once more, modulated it, it’s rising in a reasonably stiff cliff.

Bear in mind, AMD is hitting 35% natural development targets for this 12 months and reaching our objective for 20% development subsequent 12 months truly hits a $6+ EPS. Analysts have a $6 goal for 2024, however the numbers do not actually add as much as why AMD would add $0.53 to the 2023 EPS estimates and $0.93 in 2024.

The Xilinx deal did present the promise of $300 million in synergies, however AMD is more likely to see the most important upside from these financial savings via 2023. The deal closed firstly of 2022 offering loads of time to implement value financial savings this 12 months.

Look Past The Disruption

I feel the one purpose AMD is buying and selling beneath $70 after hitting $164 final 12 months is the brief sightedness of the inventory market. The chip firm hasn’t warned or reduce targets for the 12 months.

The enterprise is just forecast to proceed taking market share over the 12 months with estimates within the information middle market with market share nearer to twenty%. AMD may simply seize 50% to 75% share very quickly with Intel struggling to get the most recent chips to market.

As well as, the upcoming launch of recent GPUs has the potential to take share on this section much like what Ryzen did in CPUs and what EPYC has achieved in servers. The important thing right here is that AMD is taking market share and never impacted by the present semiconductor cycle.

The addition of Xilinx offered one other avenue to development with the FPGA chip agency clearly failing to hit demand previous to closing the deal. AMD has offered entry to higher chip provides with TSMC (TSM) boosting gross sales.

On high of all of those alternatives for present market share positive factors, the corporate is just now forging a path into the booming auto tech sector. The full addressable market is forecast to succeed in $135 billion by 2026 with the addition of the $29 billion alternative within the Embedded section from the addition of Xilinx.

Supply: AMD Q2’22 presentation

Nothing occurring proper now impacts these targets. The PC market is weak on account of covid pull forwards. The market will finally stabilize again at prior ranges with probably elevated demand on account of house and workplace wants in a extra various work away from the workplace setting.

Whether or not AMD hits the analysts consensus targets of practically a $6 EPS in 2024 or the estimates of Stone Fox Capital for a $6+ EPS in 2023, the chip firm is on the trail to far increased earnings when the present macro points are resolved. The inventory should not be buying and selling at near 11x the logical earnings stream out one or two years.

Takeaway

The important thing investor takeaway is that AMD is way too low cost right here. The market has priced in distinctive weak point that is not even more likely to occur. Traders shopping for the inventory listed below are capable of purchase shares at solely 11x earnings.