")

enigma_images/ E+ by means of Getty Pictures

Purchasing business that remain in the product packaging area might not appear like one of the most amazing means to earn a profit. However in my viewpoint, product packaging companies use several of the very best potential customers at this moment in time. One of the gamers in this area, a firm that generates pressure-sensitive products like documents, plastic movies, steel aluminum foils, as well as textiles, a lot of which are offered to identify printers as well as converters that transform stated items right into tags as well as various other offerings, is Avery Dennison ( NYSE: AVY). Historically talking, the business has actually succeeded to expand on both its leading as well as profits. About comparable companies, the supply is a little bit costly. However on an outright basis, it is still economical sufficient to price a ‘acquire’. However certainly, financial problems doubt as well as unpredictable. And also consequently, the image for any individual company or sector can adjustment at a minute’s notification. This makes it more crucial than ever before for capitalists to pay unique focus when companies report their monetary outcomes each quarter. It so occurs that, for Avery Dennison, the following profits launch will certainly get on February second prior to the marketplace opens up. Leading up to that factor, capitalists ought to understand what to anticipate as well as what to keep an eye out for.

Terrific outcomes until now

The last write-up I composed concerning Avery Dennison was released in late August of 2022. Leading up to that factor, solid sales as well as earnings had actually contributed in pressing shares of the business greater. In addition to that, monitoring was providing capitalists a much more beneficial sight of the 2022 than what they had formerly. Eventually, I wrapped up that shares of the business we’re still basically appealing as well as appealing from a cost point of view. At the very same time, nonetheless, I likewise identified that the gravy train had actually been made which additional benefit from that factor would certainly be much more minimal. This still did not avoid me from ranking the business a soft ‘acquire’, a ranking that shows my sight that shares ought to partially exceed the more comprehensive market for the direct future. While shares of the business are still up 14.3% contrasted to the 3.2% decrease experienced by the S&P 500 when I covered the company in March of in 2015, they have actually been practically level because my August write-up. Comparative, the S&P 500 has actually been up just decently, uploading a gain of 0.7%.

Writer – SEC EDGAR Information

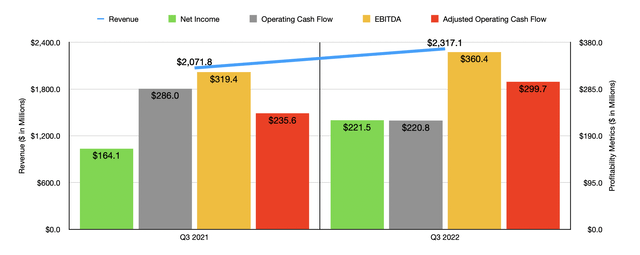

I understand I stated currently that the gravy train had actually currently been made. However fact be informed, I am a little bit stunned as well as just how minimal benefit has actually been. Take into consideration just how the business done throughout the 3rd quarter of its 2022 . Throughout that time, sales was available in at $2.32 billion. That stands for a rise of 11.8% over the $2.07 billion created one year previously. This boost, though remarkable, was not as remarkable as it needs to have been. Total sales for the Tag as well as Graphic Products section of the business took care of to climb up about 12%, increasing from $1.37 billion to $1.54 billion. However had it not been for discomfort connected with international money translation, development would certainly have been 20%. The business likewise saw a 17% increase in sales for the Retail Branding as well as Info Solutions section, with profits leaping from $541.1 million to $633.2 million. Real natural development was just 7%. In this instance, international money in fact included 5% to the section’s leading line, yet the huge motorist was a 14% payment brought on by procurements.

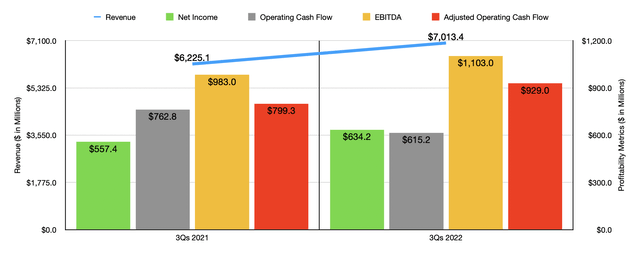

Earnings for the business likewise boosted throughout this home window of time. Earnings of $221.5 million overshadowed the $164.1 million reported in the 3rd quarter of 2021. It holds true that running capital decreased, going down from $286 million to $220.8 million. However if we change for adjustments in functioning resources, it would certainly have climbed from $235.6 million to $299.7 million. Likewise, EBITDA for the business likewise boosted, leaping from $319.4 million to $360.4 million. The 3rd quarter is just a preference of just how the business done for 2022 in its entirety. Profits of $7.01 billion was meaningfully more than the $6.23 billion reported for the initial 9 months of 2021. That earnings boosted from $557.4 million to $634.2 million. Once more, running capital took a hit also, going down from $762.8 million to $615.2 million. However on a modified basis, it would certainly have expanded from $799.3 million to $929 million. And also ultimately, EBITDA for the business boosted from $983 million to $1.10 billion.

Writer – SEC EDGAR Information

Monitoring has actually stated that modified profits per share for 2022 ought to be in between $9.70 as well as $9.85. This contrasts to the prior anticipated series of in between $9.70 as well as $10. Taking the navel, we would certainly wind up with an analysis of around $800.6 million. If we likewise presume that the various other success metrics will certainly increase at the very same price the take-home pay should, after that we ought to expect modified operating capital of $1.24 billion as well as EBITDA of $1.47 billion. However certainly, this sort of efficiency is contingent on just how the business made out throughout the last quarter of the year. Currently, experts expect profits of $2.17 billion. This would certainly contrast to the $2.18 billion business reported one year previously. This would in fact be instead shocking provided just how solid the remainder of 2022 searched for the business. When it involves profits, monitoring offered a projection for GAAP of $2.025 per share at the navel as well as a modified analysis of $2.075 per share. Experts, at the same time, are approximating that main profits will certainly be just $1.98, while the changed number would certainly be $2.03. Comparative, at the very same time one year previously, main profits were $2.19 per share, while changed profits were $2.13.

Writer – SEC EDGAR Information

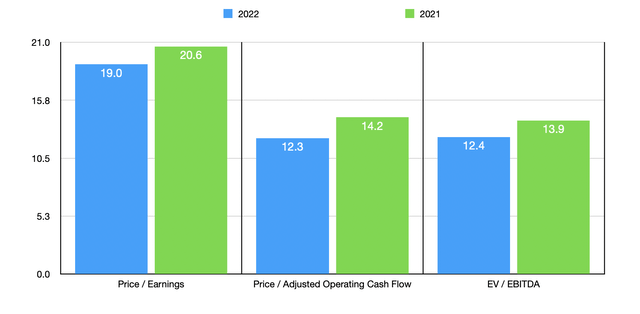

Making use of the price quotes that I currently offered, I determined that the business is trading at a price-to-earnings multiple of 19. The rate to changed running capital numerous is 12.3, while the EV to EBITDA numerous ought to be available in at 12.4. Comparative, if we were to utilize the information from the 2021 , these numbers would certainly be 20.6, 14.2, as well as 13.9, specifically. As component of my evaluation, I did likewise contrast the business to 5 comparable companies. On a price-to-earnings basis, these business varied from a reduced of 10.5 to a high of 18. And also utilizing the EV to EBITDA method, the array needs to be from 5.5 to 9.8. In both of these situations, Avery Dennison was one of the most pricey of the team. When it involves the rate to running capital method, the array was from 4.9 to 14.8. In this situation, 4 of the 5 business were less costly than our target.

Firm |

Rate/ Incomes |

Rate/ Running Capital |

EV/ EBITDA |

Avery Dennison |

19.0 |

12.3 |

12.4 |

Sonoco Products (KID) |

13.7 |

14.8 |

9.5 |

Product Packaging Firm of America (PKG) |

12.6 |

8.8 |

7.0 |

Graphic Product Packaging Holdings (GPK) |

18.0 |

9.5 |

9.8 |

Sealed Air Firm (SEE) |

13.7 |

12.1 |

9.5 |

WestRock Firm (WRK) |

10.5 |

4.9 |

5.5 |

Takeaway

Basically talking, Avery Dennison has actually been knocking it out of the park. By practically every step, the business is doing effectively. Regrettably, this has actually led the marketplace to appoint an instead high rate on shares contrasted to comparable organizations. However on an outright basis, the supply does not look expensive, although it may be a little bit soaring contrasted to its rivals. definitely, the gravy train has actually been made, yet lacking anything terrible occurring throughout the last quarter of the year, I would certainly expect that shares ought to increase a little bit greater where they are today. However certainly, this image might alter based upon the monetary information reported in the following couple of days.