After the robust rebound for the U.S. financial system in 2021, progress in 2022 has slowed within the face of rising inflation, the family earnings squeeze, and geopolitical occasions. Whereas the financial system continues to take care of elevated inflation, knowledge reveals a slowdown within the progress of business actual property. Demand for residences and workplace areas is decrease in comparison with earlier quarters.

Demand for residences and lease progress decelerates

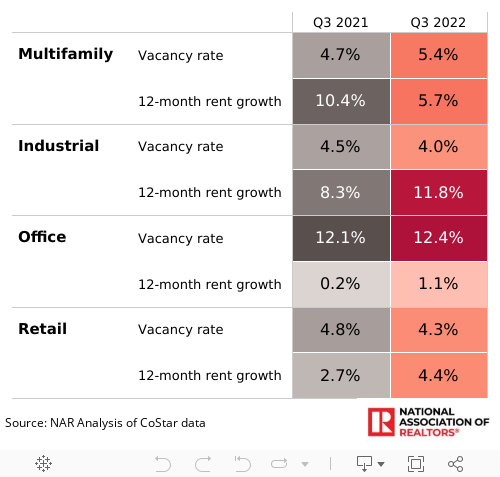

Whereas the economic growth continues to indicate no indicators of stopping, multifamily absorption and lease progress are decelerating. Multifamily absorption within the final 4 quarters was under the pre-pandemic ranges, within the vary of 60,000-70,000 items. Within the meantime, rents rose year-over-year at a slower tempo, by lower than a double-digit share for the final two quarters.

Nonetheless, authorities knowledge reveals that lease progress is accelerating. Why do not personal and authorities knowledge align? The Shopper Worth Index (CPI), which gives details about lease inflation, makes use of knowledge from the Shopper Expenditure Survey (CES) to find out the extent of costs for items and companies. Whereas this can be a survey, most renters report the lease they’ve locked in earlier. In consequence, lease modifications could take months to indicate up in authorities knowledge. In distinction, the personal sector publishes the listed rents – present lease costs. Thus, authorities knowledge will probably present a decelerating development in lease costs after a number of months.

Nonetheless, multifamily housing demand stays comparatively robust. Given rising mortgage charges and residential costs, individuals could also be pressured to lease for longer resulting from lowering affordability.

The workplace sector continues to wrestle amid hybrid work situations

Because the nation navigates hybrid work, the workplace sector continues to wrestle. In Q3 2022, about 1.34 million extra sq. toes of workplace area was vacant and positioned in the marketplace than have been leased. Though extra individuals returned to their workplaces, after 4 quarters with optimistic internet absorption, demand for workplace area dropped as internet absorption turned damaging once more. In consequence, the market’s internet demand for workplace areas decreased relative to produce, and the emptiness charge rose to 12.4% in Q3 2022 from 12.3% within the earlier quarter. In the meantime, the workplace sector has the best emptiness charge throughout all sectors of the business actual property market.

Demand for retail areas has remained optimistic for seven straight quarters

Retail gross sales – excluding fuel, auto, and non-store retailers – superior to $383 billion in August, a 19% enhance from pre-pandemic ranges (August 2019). In consequence, internet absorption elevated to 23.3 million sq. ft. within the third quarter of 2022, a 22% enhance from the second quarter. In the meantime, neighborhood retail that provides in-person companies continues to advance even sooner. Internet absorption for neighborhood facilities rose by 35 share factors in comparison with the yr’s second quarter.

The economic sector reveals no indicators of stopping

The economic sector continues to outperform. Demand is powerful as internet absorption was practically 425 million sq. ft. within the final 12 months ending in Q3 2022. Though demand could have tapered, the amount of commercial area absorbed continues to be double that of pre-pandemic instances. In consequence, this sector had the bottom emptiness charge, at 4%, of another sector within the business actual property market.

As demand stays robust, lease progress of commercial areas continues at historic highs, rising by a double-digit share (12%) in Q3 2022. In the meantime, rents are rising even sooner for logistics area by 13.5% year-over-year.

Lodge occupancy rose throughout the summer time however remained under pre-pandemic ranges

A number of elements go into evaluating the efficiency of the lodge sector. The three most prevailing measures are the occupancy charge, Common Every day Fee (ADR), and Income Per Obtainable Room (RevPAR). First, the occupancy charge reveals what number of rooms are occupied. Thus, a better occupancy charge interprets to increased demand. Second, the ADR measures how a lot income is made per occupied room, whereas the RevPAR reveals the income per obtainable room.

Information reveals that these three elements elevated within the final three months ending in August in comparison with the identical interval a yr in the past. Lodge occupancy rose to 68.7% from 66.3%; ADR elevated to $155/room from $137/room; and RevRAP went as much as $107/room from $91/room.

Nonetheless, lodge occupancy stays under the pre-pandemic stage as inflation stays elevated. Lodge occupancy was above 70% throughout the identical interval in 2019.

To summarize, the desk under reveals the emptiness charge and 12-month lease progress by sector:

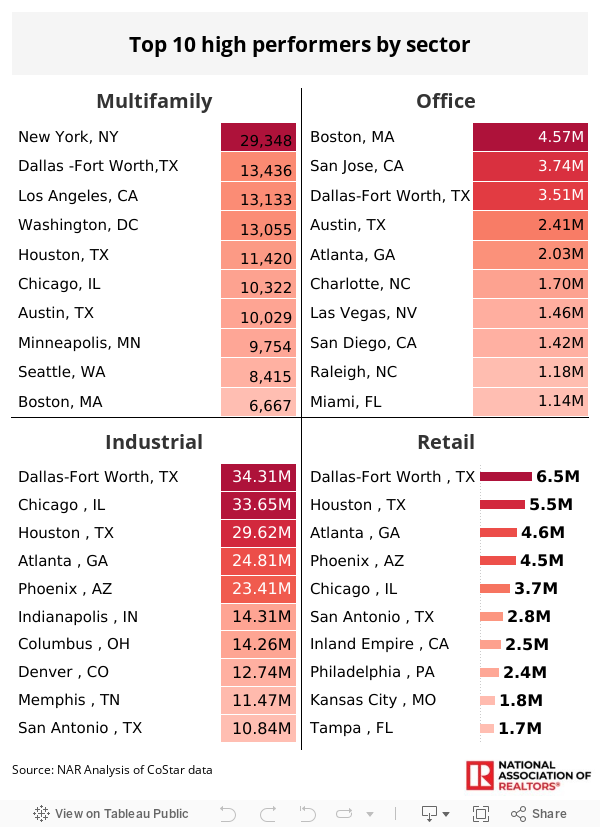

Whereas all actual property is native, business actual property carried out even higher in some areas. Under are the highest 10 areas that carried out higher by sector:

Inflation, rates of interest, provide chain woes, and geopolitical occasions are the principle elements that may decide how business actual property will carry out within the following months. The Nationwide Affiliation of REALTORS® will preserve you knowledgeable month-to-month concerning the developments on business actual property.